Gold – a geopolitical topic of great personal significance

Gold decides who holds the reins of power. The queen of value preservation cannot be corrupted and exposes the dishonesty of the West with its non-transparent and manipulated financial system. No wonder Western central bankers and private bankers avoid gold like the devil avoids holy water. Analysis

Peter Hanseler

Introduction

In my last article (“Escalation towards World War 3 – Analysis”), I spoke about the geopolitical risks that are sweeping the world. Not only the majority of the population, but also the politicians, who are opening the doors to hell with their provocations, do not perceive the situation as it is – highly dangerous.

The geopolitical dangers described are compounded by economic abysses that are covered up with false figures and forecasts and keep investors in markets that, on sober reflection, promise nothing good. The “experts” who keep investors in the financial markets with empty promises work for an industry that only makes money if the theater of speculation is sold out to the last seat. The central bankers of the West are perceived as god-like augurs who know best. However, this reputation does not stand up to even superficial scrutiny. Anyone who compares what central bankers said a few quarters ago with reality knows that central banks are not only regularly wrong with their forecasts, but practically always mistaken, and that their policies lead to a grotesque devaluation of our hard-earned money, which we hold in currencies. They do not serve the people, but a financial lobby that puts the interests of the population last.

Even the Swiss National Bank, celebrated as the guardian of the Swiss franc, is destroying our currency and is only a shadow of its former self. The gigantic profits of the last quarter, which follow disturbing losses, are the best proof that the SNB has degenerated into a hedge fund and is not fulfilling its real task – stability: We refer you to our detailed article on this tragedy “Swiss National Bank – an obituary of its former nimbus” from November 2022, where we rolled up the history of the SNB and showed how the former goddess of Swiss franc stability lost its way.

This essay attempts to show that in today’s world of turbulence, gold has the potential to be perceived again as what it has been for millennia – the true queen of value preservation.

The analysis begins with what is probably gold’s greatest strength – the fact that gold is not exposed to counterparty risk if it is held in its basic form – physically. After that, we’ll be debunking the arguments against gold and explaining why the financial industry hates gold like the devil hates holy water.

Gold is money – everything else is credit

At a hearing of the US Congress in 1912, John Pierpont Morgan – probably the most powerful banker of his time – made the following statement about gold:

«Gold is money – everything else is credit»

John Pierpont Morgan – 1912

This statement summarizes all the arguments that make up gold. At first glance, this sentence seems difficult to understand. However, if you understand the term “counterparty risk”, you realize that J.P. Morgan made a statement that should be the basis of every investment decision if you do not want to be confronted sooner or later with the realities that you would have avoided if you had recognized them.

Counterparty risk

Introduction

In order to understand the greatest advantage of gold over almost all other assets, you need to understand the concept and system of “counterparty risk”. This is much simpler than you might think. The chain of counterparty risk stretches from the tradesman to the central banks. Financial losses and debacles very often have the same cause: in a transaction, the party that suffers losses has misjudged its counterparty and thus misjudged the counterparty risk.

Craftsman

A painter paints a customer’s apartment and is left with an unpaid invoice. He has misjudged the customer’s willingness to pay the invoice.

Credit risks of the banks

In March 2021, Credit Suisse lost five billion because it had granted a huge loan to the American “Archegos” fund, which speculated on the money and was unable to repay it. The bank had misjudged the risk and the money went down the drain. This debacle was the first step on the road to Credit Suisse’s downfall.

Bank customer

The counterparty of the investor is the bank. Most bank customers refer to their account as “their” money. However, this is wrong: the money belongs to the bank, because ownership of the money is transferred to the bank the moment the customer deposits the money into the bank and all that remains for the customer is a contractual claim that obliges the bank to return the money to the customer.

The bank also has no obligation to keep the entire amount safe, only a fraction of it; this is regulated by law. The bank can play with the rest: Grant loans, invest without telling the customer what it is doing with the money – it can do this because the money no longer belongs to the customer. In return, the customer receives an interest rate that regularly does not even compensate for inflation. A miserable deal for the customer, who gets nothing and risks everything.

To put it simply, this works until around 10% of customers make a claim at the same time and demand their money back. If this happens, it is called a “bank run” and the bank goes bust.

If this happens, the customers have misjudged the risk and the money or the claim to it is gone. Aware of this risk, many countries have a regulation that a certain amount is guaranteed by the state. In Switzerland, this amount is CHF 100,000 per customer.

Cash

If you hold your assets in cash, i.e. in banknotes, you avoid the risk described above of your bank going bust, but you still have a counterparty risk: the central bank. If you hold Swiss francs, the Swiss National Bank (SNB) is responsible; if you hold US dollars, you are at the mercy of the US Federal Reserve Bank (Fed).

A central bank cannot go bankrupt because it can print the currency it issues indefinitely and so it is theoretically impossible to lose everything as the holder of a banknote. I use the word “theoretically” because it is possible in practice and has happened many times.

The best-known historical example of this is the German Reichsmark, which completely lost its value in 1923 during the so-called Weimar hyperinflation. On November 1, 1923, a banknote of 5 trillion Reichsmarks, i.e. 5,000 billion (5,000,000,000,000,000.-) had the same purchasing power as a 50 mark note in 1914. How could this happen?

“Even the Swiss National Bank (SNB) is anything but a hero in maintaining the value of the Swiss franc”

With the outbreak of the First World War, Germany suspended the gold standard, i.e. until then the paper money issued by the Reichsbank was backed by its gold reserves. It was decided to decouple the Reichsmark from gold in order to be free to print money for war expenditure. This was the beginning of the end and more and more money was printed, which led to the collapse of the Reichsmark five years after the end of the First World War.

The Swiss National Bank (SNB) is also anything but a hero in maintaining the value of the Swiss franc, although it does this better than any other central bank in the world. Please refer to my article on the SNB.

It is not at all difficult to prove that the SNB does not deserve the status of hero in maintaining value. The SNB does it better than the other central banks and can be described as the one-eyed man among the blind.

Cash compared to gold

Let’s take a typical Swiss example: In 1949, a girl receives a 20-franc gold Vreneli from one of her grandfathers for Christmas and a 20-franc banknote from the other to save. Both have a value of CHF 20.

Delighted with the large gifts, the child puts the banknote and the Vreneli into her piggy bank and puts it to work.

If the girl, who has become an old woman, butchers her piggy bank today, the CHF 20 banknote will still have a value of CHF 20, if the bill can still be exchanged at all; the gold Vreneli, however, has a value of over CHF 400. From a gold perspective, the Vreneli has not increased in value, but the franc has lost over 95% of its value. So much for the stable Swiss franc.

The counterparty risk when holding cash is therefore that the central bank does not protect the value of the money, but destroys it.

Risk of central banks among themselves

The last link in this chain of risks is the central banks themselves. The Russian central bank became aware of this risk in 2022.

Western countries, above all the US, the EU and Switzerland, blocked the Russian central bank’s foreign currency reserves of around USD 300 billion. As Russia has no net debt and invests a considerable proportion of its reserves in gold, this sanction did not have the effect desired by the West, namely the collapse of the Russian economy. The indirect effect of this blockade, which will have historical consequences, is discussed below.

Interim result

The greatest advantage of physically held gold is therefore that it is not exposed to the counterparty risks described above. The only risk a person has if they hold gold physically is theft. Scrooge McDuck can tell you a thing or two about it.

The quote from J.P. Morgan, “Gold is money, everything else is credit”, is therefore a very wise sentence; you just have to understand it.

Paper money – nowadays more widely used electronic money – is therefore fraught with risks that most people are not aware of. If your grandfather asks you whether you would prefer cash or gold, this question is now very easy to answer.

Bogus arguments against gold

Most bankers, investors, central banks and governments put forward arguments against gold. On closer inspection, however, these are bogus arguments and most of them are simply wrong.

Gold yields no interest

This argument is not an argument against gold, but for it. Gold is money and money – as long as it is held in cash – does not yield interest. There is only interest on money when it is invested, i.e. taken to the bank. But then the counterparty risk described above comes to life.

Gold is a poor investment

This is the bankers’ favorite argument, but it is not only nonsensical, it is also wrong.

Nonsensical because physical gold is not an investment, but money.

And wrong because the figures speak for themselves. By way of comparison, let’s pit the world’s largest share index, the US S&P 500, which tracks the 500 largest listed US companies, against gold. We look at the performance over two periods: The first period is supposed to be a long one: from January 1, 2000 to today, May 17, 2024. The second period is supposed to be a short one, the current year 2024.

S&P 500 performance if all dividends on the shares are reinvested

Period 01.01.2000 – 05.17.2024: 453%

Period 01.01.2024 – 05.17.2024: 5.53%

The bank’s costs and fees must be deducted from this performance.

Performance Gold (no dividend)

Period 01.01.2000 – 05.17.2024: 843%.

Period 01.01.2024 – 05.17.2024: 16%.

This refutes the most popular argument against gold, because bankers always put forward arguments that were valid in a world that no longer exists. As a saver, I am not interested in what happened 70 years ago. So, in my opinion, a look back over twenty years is more helpful and more true to life.

“The grandmother who keeps her savings in gold beats the banker hands down”

The interests of bankers run counter to the interests of clients

The bankers have every reason to lie and advise you not to buy gold; this is anything but surprising and the reasons are as obvious as they are trivial. When you buy physical gold, the banker earns nothing. In the buying process, the banker earns minimally and once you store the gold in a safe or under your mattress, the banker’s income dries up completely.

The interest of a bank is to make money – the interest of the customer is secondary at best. If banks thought about their customers, they would compete with each other on the performance of customer deposits and thus advertise their own performance. Have you ever seen a bank that advertises the performance of its client portfolios?

Western central banks

Western central banks hate gold. And they have done so since 1971 when President Nixon abolished the gold standard. I have already written about this several times in the articles “Endgame of the petrodollar“, “The unstoppable rise of the East” and “Swiss National Bank – an obituary of its former nimbus“.

Gold is hated because its value is the purest illustration of the destruction of our paper currencies. Since 1971, the US dollar has lost 98% against gold, the Swiss franc “only” 90%.

Interim result

Holding gold instead of investing in shares, for example, therefore has major advantages: Gold retains its value and is not exposed to counterparty or market risk, because gold does not fluctuate. But everything around gold goes up and down and everyone wants to buy low and sell high, with very mixed success.

The grandmother who holds her savings in gold has thus beaten the banker hands down, not only in the last 24 years, but also in the current year.

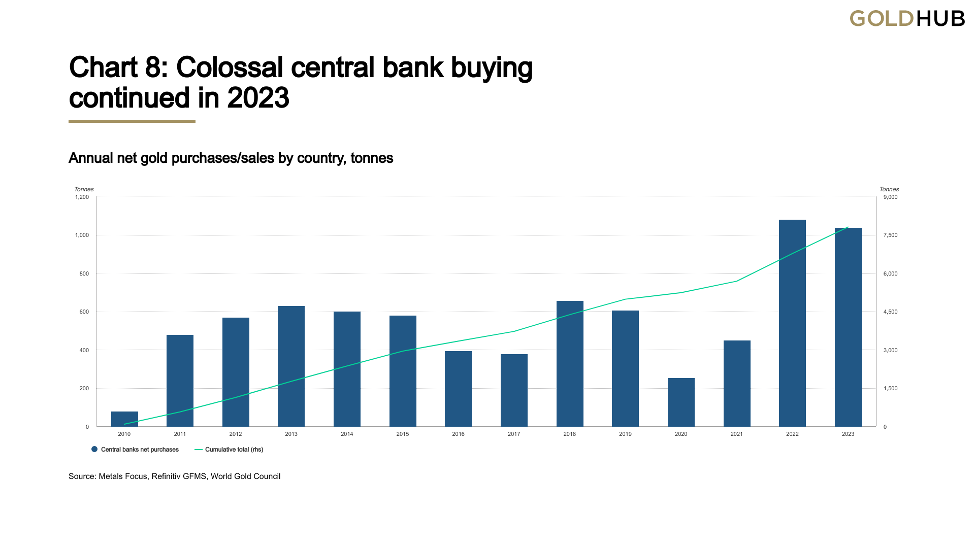

Central banks buy a lot of gold

Facts

Looking to the future begins in the present. In recent years, central banks have practically maintained their gigantic purchases of 2022.

There are many reasons for this. Some of them will be discussed.

Central banks protect themselves against currency devaluation

The huge purchases of gold by central banks are on the one hand a consequence of the irresponsible behavior of major central banks. Since 2008, the Fed, the ECB and the Japanese central bank have been printing money that takes your breath away; this has led to a major devaluation of these currencies. By buying gold, the buying central banks are protecting themselves from this danger; see my comments in the articles “BRICS – the project of the century“, “Endgame of the petrodollar” and the SNB for more details.

Central banks around BRICS turn away from the US dollar

In the past, the world’s central banks bought US government bonds as they held their reserves in US dollars because all commodities were settled in this currency and the economy therefore needed US dollars. For some time now, however, there has been a tendency for many countries surrounding the BRICS organization to move away from the US dollar, conduct their business in their own currencies and thus increasingly hold gold again.

In our comprehensive article “BRICS – the project of the century“, we discussed in detail the overall development of BRICS and the negative impact on intrinsic value. A chart published by Bloomberg speaks volumes: the use of the US dollar as a reserve currency has been collapsing since 2022. The graph does not yet show any figures for 2023, but I assume that the trend will continue.

Central banks around BRICS fear expropriation

Central banks are also exposed to the aforementioned counterparty risk. With the stroke of a pen – decided by a few politicians – Russia’s foreign currency reserves were frozen due to its military intervention in Ukraine and on April 23, 2024, the US Congress passed the so-called REPO Act, under which the President is allowed to seize Russian state assets under the jurisdiction of the United States to support Ukraine.

“The Chinese, who hold over 3,246 billion US dollars in reserves, were shocked”

The freezing and now also the confiscation worked without any problems because, for example, the US dollar reserves of the Russian Central Bank are not held in Russia, but at the Federal Reserve in Washington. This works in exactly the same way as when a bank customer holds a USD account with their bank in Switzerland: The money is in America and the Swiss bank only has a claim on the US dollars. A central bank that holds foreign currencies is therefore just as exposed to the other central banks as the bank customer described above. Politicians have exploited this situation and robbed the Russian central bank of its funds.

The Chinese, who hold over 3.246 billion US dollars in reserves, are shocked by the West’s actions against Russia. They are probably wondering whether the same will happen to them. If you follow the Western media, you can see that the negative propaganda is increasingly turning against the Chinese as well, after years of focusing on the Russians. Now the Western politicians – with the knowledgeable help of their media – just have to raise the outrage against China a few more notches and then the Chinese can also have their foreign currency reserves frozen.

The Chinese have been buying gold for decades in order to escape the US dollar and its devaluation. Since this year, they have been additionally motivated by the freezing of Russia’s foreign currency reserves. They probably also bought the most in 2023.

The chatter of central bankers

Equities are overvalued, real estate is overvalued, bonds are overvalued, inflation is raging to an extent rarely seen before and the central banks’ chatter is unbelievable: when inflation began – well before the war in Ukraine – Jerome Powell, Chairman of the US Federal Reserve, and Christine Lagarde, President of the ECB, claimed that inflation was temporary. That was incorrect. Incidentally, this was not an isolated case; central bankers in the West are traditionally among the lousiest forecasters when it comes to money and the economy. The fact that people still believe them is beyond me.

Why is the gold price not moving more strongly?

Gold has put in a great performance so far in 2024 in Swiss francs, gold has risen by 25% to date, while the Swiss benchmark index SMI has only risen by 8%.

“That makes about as much sense as if the price of bread were determined by the price of the paper wrapper in which the bread is wrapped”

However, according to the law of supply and demand, the price of gold should have risen much more strongly in recent years – what is wrong with that?

The problem is that the price of gold is not determined on the physical market, but by the LBMA in London and the Comex in New York. No physical gold is traded on these markets, but so-called paper gold; these are stock exchanges that trade derivatives backed by only a fraction of a percent of physical gold.

The pricing practiced in the West makes about as much sense as if the price of bread were determined by the price of the paper wrapper containing the bread. This is not a fault of the system, but intentional.

Central banks have been trying to keep the price of gold low since 1971 – I have already discussed this. There are even telephone transcripts of conversations between President Nixon and his Secretary of State Kissinger in the fall of 1971 that prove this.

Although the gold price in US dollars has risen from USD 35 in 1971 to over USD 2,300 today, attempts have been made for 50 years to depress the gold price through market manipulation.

From conspiracy theory to reality

Until recently, allegations of market manipulation were relegated to the world of conspiracy theories. However, four years ago, the largest player in these markets, the American bank J.P. Morgan Chase, was fined USD 920 million for market manipulation in the precious metals market.

“Of course, this had no further consequences for the gentlemen in the carpeted floors of this criminal bank”

This bank was found to have manipulated the market through spoofing. Spoofing describes the activity of falsely misleading the market into believing that one wants to make huge purchases or sales in order to encourage other market participants to buy or sell, which pushes the price up or down. However, these purchases or sales by the spoofers are withdrawn at the last moment and the spoofers then buy or sell a position before the market realizes that it has been ripped off. The other market participants foot the bill.

Experts explain that the USD 920 million fine was a mere pittance compared to the sums that JP Morgen had earned through this scam.

Of course, this had no further consequences for the gentlemen in the carpeted floors of this criminal bank.

Prospects

If you look at the advantages of gold and are aware of the fact that Western central banks are manipulating the price of gold downwards, but the rest of the world is buying more and more gold and turning its back on the US dollar, gold is already very attractive as an investment from this perspective.

The market turbulence in almost all other asset classes such as equities, bonds, real estate and cryptocurrencies also speaks in favor of gold.

“We should be more afraid of the banks than the Beagle Boys”

We have also discussed why the banks are not giving this advice. You should be more afraid of the banks than the Beagle Boys.

This article is not a recommendation to buy, but an appeal to common sense. I am merely recommending what I do myself.

If you decide to buy, buy physical gold and keep it in a safe, not at a bank, but at a gold dealer or at home and not all in the same place. Banks will offer you gold accounts, ETFs and other products. These have one thing in common: they are expensive and have a counterparty risk, which we have discussed in detail in this article.

Our blog does not advertise and we do not enter into any agreements with providers. We therefore make the following recommendations without any vested interests and therefore completely independently.

I personally and many of my friends buy gold through ProAurum. ProAurum is one of the largest gold dealers in Switzerland (ProAurum-Switzerland) and Germany (ProAurum-Germany) and I am impressed by their reliability, good service and fair pricing. You can collect your precious metals from ProAurum at the counter, store them in a safe at ProAurum or in ProAurum’s large vault. For silver purchases that are subject to VAT, ProAurum also offers storage in a duty-free warehouse.

Because of my work, I also know reliable people who can advise you on purchases outside Switzerland or Germany. You are welcome to contact me personally in this case and I will simply forward your request.

21 thoughts on “Gold – a geopolitical topic of great personal significance”